As a financial advisor and planner, I help people reduce their tax liability over the course of their life. While this is a core tenant of financial planning, it’s also one that’s frequently overlooked.

This article is crafted to ensure you comprehend what tax liability refers to, delving into its intricacies and examining how various aspects of your financial situation combine to determine your obligations to the government.

Together, we’ll look at various financial planning strategies you can use to reduce your tax burden as well as the importance of seeking professional guidance to make the most of your savings.

What Is Tax Liability And What Impacts It?

Understanding tax liability is critical for sound financial planning. It’s not just about your income level; it’s about grasping the nuances of how various income types, such as salaries, investments, and other earnings, are taxed and when. Your tax bracket is crucial here, as higher income often means a higher bracket and, therefore, greater tax liability. For high-income earners, specific tax planning strategies can offer substantial benefits.

Taxable income is another key factor. Utilizing tax deductions, like those for retirement savings, mortgage interest, and business costs, can significantly reduce your taxable income, thereby lowering your tax obligation. Tax credits, which reduce your tax bill on a dollar-for-dollar basis, offer another layer of savings, distinct from deductions. The status of your filing (e.g. married, single, qualifying widow(er), or head of household) also influences your tax rates and available deductions.

Finally, your employment status and state-specific laws play a substantial role. The tax implications vary for self-employed individuals, full-time employees, or part-time workers. State laws contribute additional complexity, governing state income tax rates, exemptions, and how different income types are taxed, as well as other taxes like property and sales taxes. Navigating these intricacies is crucial to effectively manage your tax responsibilities and maintain financial health.

What Is Financial Planning?

Financial planning is a strategic approach some advisors use to help you achieve your financial goals. It involves creating a comprehensive plan tailored to your unique circumstances. As a CFP® Professional, I focus on several key areas to guide you effectively:

Retirement Planning: This is about ensuring you have the funds to live comfortably after you retire. Retirement planning helps you understand various retirement savings options, assess your future needs, and create a plan that grows with you and protects you.

Investment Management: Proper investment management is pivotal for wealth accumulation. It’s a personalized investment strategy that brings your personal financial goals, risk tolerance, and time horizons into alignment.

Risk Management/Insurance Planning: Risk Management/Insurance Planning is about protecting your wealth. It’s an assessment of your needs to make sure the right coverage—be it life, health, auto, property, or umbrella insurance—is in place to safeguard your (and your family’s) financial future.

Estate/Legacy Planning: This process is conducted to ensure your assets are allocated according to your preferences once you pass away. It involves creating a detailed strategy, encompassing wills and trusts, aimed at reducing taxes and legal complications for your beneficiaries. Ultimately, you want as much of your wealth as possible to go where it’s important to you after you’re gone and as little as legally possible to go to taxes.

Tax Planning: A commonly overlooked yet vital part of financial planning is reducing tax liability. It aims to help you understand lifetime tax consequences, uncover avenues for future tax savings, and leverage various tactics to decrease your overall tax obligations throughout your life.

Financial Planners and Accountants

As a Certified Financial Planner (CFP®), I focus on the broader aspect of your financial health, including long-term tax planning. My role as a financial advisor is akin to a long-term financial coach, developing strategies that aim to reduce your tax liabilities over your lifetime. I look at the big picture, considering factors like retirement planning, investment strategies, and estate planning to create a comprehensive approach that can lead to significant tax savings in the long run.

Conversely, a Certified Public Accountant (CPA) is a tax authority that specializes in the intricacies of annual tax preparation and filing. CPAs are proficient in the latest tax laws and regulations, making sure that you benefit from all available deductions and credits each year. Their expertise is invaluable for maximizing your tax efficiency on an annual basis, helping you save on taxes annually by meticulously managing your tax returns.

In practice, CFP®s and CPAs serve complementary roles in managing your taxes. While I, as a CFP®, guide you through long-term strategies to minimize your lifetime tax bill, a CPA ensures you reap immediate tax benefits each year. Together, we can create a robust tax strategy that aligns with both your short-term and long-term financial goals, helping you pay the least amount of taxes as legally possible at all stages of your life.

Please note: At Snowpine Wealth, we’re happy to work alongside your CPA or recommend one from our network. This collaboration ensures you are fully equipped to handle taxes both annually and over your lifetime. If you’re looking to optimize your tax situation comprehensively, schedule an appointment using the button below to explore how we can work together to maximize your tax savings.

What Happens To Your Tax Liability With Proper Financial Planning?

By leveraging the right financial planning strategies, you can drastically reduce your lifetime tax bill. In this section, I’ll walk you through various approaches that you can use to your advantage.

That said, it’s important to remember that financial planning and tax strategies aren’t one-size-fits-all solutions. Everyone’s tax planning needs are different, but the following strategies are core components I often discuss with clients to tailor a plan that aligns with their unique financial situation and goals.

Reducing Tax Liability With Retirement Savings

Retirement planning is one of the most important parts of financial planning, specifically aimed at reducing your tax liability. By thoughtfully investing in retirement accounts, you can reduce your taxable income both now and in the future. Here’s how financial planning can effectively reduce your tax liability through retirement savings:

Employer-Sponsored Retirement Plans: Participating in plans like 401(k)s or 403(b)s allows for pre-tax contributions, which can lower your taxable income. Some employers even offer matching contributions, enhancing your savings potential.

Roth and Traditional IRAs: These individual retirement accounts offer unique tax benefits. Traditional IRAs provide growth that is tax-deferred and contributions that are tax-deductible, while Roth IRAs offer both tax-free growth and withdrawals.

Calculated Withdrawals From Accounts: Careful scheduling of withdrawals can help in reducing tax liabilities. Understanding the optimal timing and amount for withdrawals from different accounts can improve your tax situation substantially during retirement.

Roth Conversions: Converting a traditional IRA to a Roth IRA involves paying taxes on the converted amount now, in exchange for tax-free withdrawals later. This strategy can be beneficial if you expect to be in a higher tax bracket in the future.

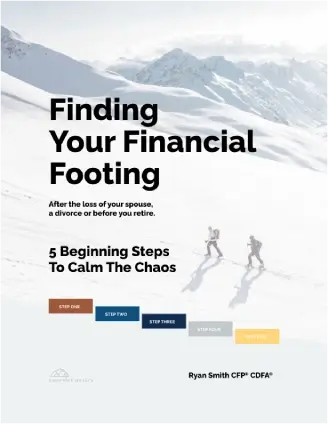

Keep in mind that retirement planning is not static. It’s a process that will continually evolve to meet your changing financial needs. By working with a financial thinking partner you can make sure you’re on the right track for your ideal next chapter. If you’re unsure about where you stand in relation to your financial future, download our free guide.

If you’re looking for financial guidance during a difficult time, but you’re not ready to schedule a call with us, we recommend our free guide:

Finding Your Financial Footing

It reveals 5 clear steps to calm the chaos before you retire.

Reducing Tax Liability With Credits and Deductions

In my role as a financial advisor, I often emphasize the importance of understanding and utilizing tax credits and deductions as a means to reduce your overall tax liability. Both can be powerful tools in your overall financial planning strategy. These are just a few that you may have at your disposal:

Tax Loss Harvesting: This involves selling investments at a loss to offset what you’ll owe in capital gains tax while keeping investments invested to take advantage of growth during volatile times. It’s a powerful tactic for managing your investment portfolio while reducing taxes.

Business Expenses: If you own a business, many expenses can be deducted, such as costs for equipment, supplies, and certain types of insurance. Proper documentation and categorization are key.

Mortgage Interest Deduction: Homeowners have the option to deduct mortgage interest payments from their taxable income. This can lead to substantial reductions, especially in the initial years of a mortgage when the interest is often at its peak.

Student Loan Interest Deduction: The interest paid on student loans is frequently deductible, which helps in lowering taxable income. This benefit is particularly advantageous for new graduates or individuals in the early phases of their professional lives.

Philanthropy: Charitable giving not only benefits society but can also reduce your tax bill. Donor-advised funds have become a popular method, allowing you to batch charitable contributions (i.e. give multiple years’ worth of donations in a single year) to help maximize deductions at an opportune time. There are also Qualified Charitable Deductions (QCDs) that you can make from your IRAs once you reach 70 ½ years old.

Please Note: Working with a Certified Public Accountant (CPA) can also be a wonderful resource in making the most of your deductions and credits. A CPA can provide specialized advice tailored to your unique financial situation. If you’re a business owner, check out our article on the 9 Empowering Questions You Can Ask Your CPA to garner insights into how you may be able to lower your tax liability further.

Reducing Tax Liability With Other Savings And Income

Understanding how to use other savings and income sources can be a game-changer in reducing your tax liability. Consider the following ways you may be able to lower your tax bill:

Flexible Spending Accounts (FSAs): FSAs enable you to allocate pre-tax income for qualified medical and dependent care costs. By doing so, your taxable income is reduced, potentially leading to considerable tax reductions.

Health Savings Accounts (HSAs): HSAs are highly beneficial for individuals with high-deductible health insurance plans. They allow for tax-free contributions and growth. Better yet, they also provide tax-free withdrawals for eligible medical expenditures, offering a one-of-a-kind triple-tax advantage.

Properly-Timed Social Security: Strategizing the timing and method of taking your Social Security benefits can impact your tax liability. For instance, delaying benefits can increase your future payments and potentially reduce taxes on these benefits.

Reducing Tax Liability With Estate Planning

To effectively reduce tax liability, it’s also important to understand the process of estate planning. Effective estate plans can protect your legacy and minimize the tax burden on your beneficiaries:

Trusts: Establishing trusts can be a key strategy in estate planning. Trusts can help manage and protect assets, minimize estate taxes, and provide for beneficiaries in a tax-efficient manner. There are also several types of trusts, such as irrevocable life insurance trusts (ILITs), grantor retained annuity trusts (GRATs), and charitable remainder trusts (CRTs) that may or may not be relevant to you depending on your estate and tax planning needs.

Annual and Lifetime Gifting: Utilizing annual gift tax exclusions allows you to give a certain amount to as many individuals as you wish each year, tax-free. Additionally, lifetime gifting can reduce your taxable estate by distributing assets during your lifetime.

Please Note: At Snowpine Wealth, we’re happy to collaborate with your estate planning attorney or recommend one of our own. Together, we can devise an estate planning strategy that’s both financially and legally sound.

Let Us Help You Lower Your Tax Liability With Proper Financial Planning

At Snowpine Wealth, my extensive experience over the past 10+ years has been dedicated to helping clients understand and navigate the intricacies of tax liability as an integral part of their financial planning. Recognizing the importance of minimizing tax liability is key to not only saving money but also unlocking your full financial potential and securing a more stable future.

Handling tax liability with proper financial planning involves more than just crunching numbers. It’s about creating a strategic approach that encompasses your retirement, investments, and legacy planning. This is where collaborating with the right professionals becomes crucial.

I can work hand-in-hand with you and either collaborate with your current CPA or connect you with one of our trusted accountants. This partnership is vital in ensuring a comprehensive approach to your financial health and in effectively reducing your tax burden.

Don’t let taxes be a burden any longer! Take control of your financial future today. Click the button below to book an appointment with me, Ryan Smith CFP®. Together, we can develop a personalized plan to minimize your taxes and maximize your financial well-being.

If you would like us to guide you through this difficult moment instead of going through it alone…

We offer a free consultation called…

The Financial Transition Strategy™

It’s designed to help you quiet the noise and create a clear path forward, as well as help you get to know us and see if we’d be a good fit to work together.

We’re always respectful, and there’s never any pressure.

Securities and advisory services offered through Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Advisor. Fixed insurance products and services not offered through Commonwealth Financial Network®.

Snowpine Wealth Strategies does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.