Personal finance connects deeply with our actions, feelings, and thoughts. Your actions significantly impact your financial success. How you spend, save, and invest directly affects your financial health.

In this post, we’ll explore how behavior influences personal finance. We’ll be taking a deeper look at the psychology of money, spending habits, saving and investing, managing debt, setting financial goals, and the link between finances and mental health.

The Psychology of Money

Behavioral finance studies how our decisions with money are influenced by our psychology. It explains why we often act irrationally with our finances. Thankfully, understanding these behaviors can help us make smarter choices. Consider the following:

Common psychological biases: We all have biases. Overconfidence leads us to think we know more about money than we do. We fear losing money more intensely than we enjoy making it due to loss aversion. Herd behavior makes us follow the crowd, even when it’s not the best move. The point is, there are several key biases that impact your investment decision making, which is why it’s so important to bring awareness to your mental tendencies.

Emotion-Driven Decisions: Emotions like fear and greed heavily impact financial choices. Fear can make us pull out of investments too soon. Greed can push us into risky ventures. Recognizing patterns of emotional investing helps us make more informed financial decisions.

Short-Term Thinking: We often seek instant gratification, ignoring long-term benefits. This mindset can lead to impulsive purchases and disregard of longer-term goals. Focusing on long-term rewards promotes financial stability.

Resistance to Change: We tend to stick with familiar habits, even if they’re harmful. This resistance, known as behavioral inertia, can block better financial strategies. Embracing new approaches can boost our financial health.

Impact of Financial Stress: Money worries can harm our mental well-being and lead to poor decisions. Stress might cause overspending or avoiding debt issues. Managing stress through mindfulness or other techniques can improve financial behavior.

Role of Social Influences: Our family and friends affect our financial choices. We often mimic their spending and saving habits. Being aware of these influences helps us make better independent decisions.

Please Note: Understanding your money personality is instrumental in understanding why you do what you do with your finances. If you’re interested in taking a deeper dive to understand your personal relationship to money, check out our guide figuring out your money personality by clicking the button below.

Spending Habits

Our spending is often driven by emotions and habits. Emotional triggers can cause us to make unplanned purchases. When we’re feeling stressed or excited, we might buy things we don’t need. This behavior can negatively impact our financial health. Recognizing these triggers and taking a moment to think before buying can help.

Moreover, when our income increases, our spending often does too. This is known as lifestyle inflation. It can prevent us from saving money. Instead of improving our finances, we end up spending more. Prioritizing saving and living within our means can help combat this.

Strategies for Managing Spending

Controlling expenses requires effort and practical tools. Here are some strategies to help you manage your spending:

Creating a budget: A budget helps you keep track of your spending and prevents overspending. It’s a straightforward tool for managing your money. Regularly updating your budget ensures it aligns with your financial goals and changing circumstances.

Tracking expenses: Recording every purchase helps you see your spending patterns. This awareness is the first step to improving the management of the money that goes out. Use apps or notebooks to track expenses, making it easier to clarify and get rid of unnecessary costs.

Mindfulness techniques: Being aware of your spending habits can reduce unnecessary purchases. Waiting a full day before making a purchase can curb impulse buys. Ask yourself if the purchase aligns with your financial goals.

Setting spending limits: Setting limits for different categories, like groceries or entertainment, can help manage your spending. Sticking to these limits requires discipline but can significantly reduce overspending and help in achieving financial stability.

Automating savings: By opting for a percentage of your income to be automatically put inside a savings account, you guarantee regular contributions. This strategy curtails the temptation to spend and steadily grows your savings.

Financial Precautions

To stay financially healthy, it’s also important to be aware of potential pitfalls and prepare for unexpected expenses. Make sure to account for the following:

Impact of High Interest Rates: High interest rates on credit cards and loans can quickly lead to more debt. It’s crucial to understand these rates and avoid carrying balances that incur high interest. Paying off more than the minimum required on credit cards can significantly hasten your journey to being debt-free.

Establishing an Emergency Fund: A dedicated savings account for emergencies provides a crucial financial buffer for unforeseen expenses. This fund is essential for preventing new debt and should ideally cover living costs for three to six months.

Avoiding Impulsive Purchases: Taking a moment to reflect before buying something can save money. Ask yourself if the purchase is necessary or if it’s momentary emotions calling you to buy. Implementing a waiting period before making significant purchases can prevent buyer’s remorse.

Understanding financial products: Being well-informed about the financial products you use, such as loans, credit cards, or investments, can prevent costly mistakes. Knowing the terms, interest rates, and potential fees helps in making better financial decisions.

Saving and Investing Behavior

How we approach saving and investing has a major impact on our financial well-being. Our habits in these areas can shape our financial future:

The Importance of Saving: Saving is crucial for financial security. It provides a buffer for emergencies and helps you achieve your long-term goals. Setting up a savings account and regularly putting money aside can make saving a regular part of your financial routine.

Investment Decisions: Behavior significantly affects investment choices. Different people have different levels of risk tolerance. Some prefer low-risk, steady returns, while others are comfortable with higher risks for potentially higher rewards. Understanding your risk tolerance is key to making wise investment choices. Making informed financial decisions ensures better outcomes in investing.

Long-term vs. Short-term Thinking: Thinking long-term is essential for financial growth. Long-term investing means focusing on future benefits and being patient. This approach helps build wealth over time. In contrast, short-term thinking can lead to hasty decisions that might not be beneficial in the long run. Balancing both views can improve financial results.

Balance Saving Investing: Balancing saving and investing is important. Saving offers a safety net, but investing allows your money to grow. By diversifying your portfolio, you can mitigate the risks associated with market volatility. Regularly evaluating your investments ensures they stay in line with your long-term financial goals.

Debt Management

Managing debt properly is essential for maintaining good financial health. Debt often builds up due to poor spending choices and lack of awareness. Impulsive purchases and not having a budget can quickly lead to debt. Taking inventory of your habits is the first step to preventing debt.

Additionally, carrying a lot of debt can harm your financial health. It can cause a lot of financial stress, making it hard to meet monthly payments and save for the future. Debt can also lower your credit score, affecting your ability to borrow money later.

Effective Debt Management Strategies

To manage debt, start by creating a repayment plan. List all debts, interest rates, and minimum payments. Focus on paying off high-interest debts first to reduce the amount you pay in interest. Avoid new debt by controlling spending and sticking to your budget.

Grasping Interest Rates: Understanding the interest rates on your debts is essential, as higher rates can make it challenging to reduce your balance. Seek to negotiate lower rates with creditors or look into consolidating your debts into one loan with a more favorable interest rate.

Paying Beyond the Minimum: Strive to contribute more than the minimum payment on your debts whenever possible. If that isn’t feasible, ensure you at least cover the minimum to avoid incurring extra fees and penalties.

Try the Snowball Strategy: Begin by paying off your smallest debts first while keeping up with the minimum payments on your larger debts. Once a small debt is cleared, start tackling the next smallest debt. This method provides early wins, fostering a sense of achievement and encouraging steady progress in your debt management journey.

Automate Your Repayments: Scheduling automatic payments guarantees that you never miss a due date. By automating your debt repayments, you avoid late fees and penalties, maintaining consistent progress and simplifying your financial management.

Financial Goals and Planning

Achieving financial goals requires planning and discipline. Clear objectives serve as a guide, helping you decide where to allocate your funds. Whether it’s buying a house, saving up for college, or preparing for retirement, having specific goals helps you stay focused.

Consistency and discipline are crucial. Regularly review your progress and make necessary adjustments. Adapting your strategies to fit new circumstances keeps your goals within reach.

Tools for Effective Planning

Using the right tools can make reaching your financial goals easier. These resources help you stay organized, track progress, and make informed choices:

Apps: Budgeting and financial planning apps help track spending and savings. They provide real-time updates and reminders, making it easier to manage your finances daily.

Accountability Partners: By confiding your goals to a dependable friend or family member, you gain both support and motivation. Their involvement can help you maintain your commitment and offer new insights into your financial decisions.

Educational resources: Books, courses, and online articles increase your financial literacy. Staying informed helps you make better financial choices and stay updated on best practices and opportunities.

Financial planners: Professional advisors offer tailored advice and create detailed plans. Choosing a fiduciary with a CFP® (Certified Financial Planner) designation is important. They are legally required to act in your best interest, ensuring their guidance is unbiased and reliable.

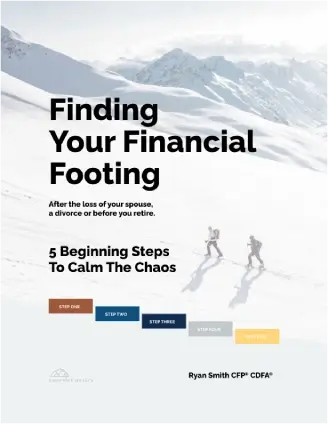

If you’re looking for financial guidance during a difficult time, but you’re not ready to schedule a call with us, we recommend our free guide:

Finding Your Financial Footing

It reveals 5 clear steps to calm the chaos before you retire.

Emotional and Mental Health

Your financial well-being is closely tied to your emotional and mental health. Good money management can reduce stress and boost happiness. Let’s take a close look at how your money and mental health are actually intertwined..

The Link Between Finances and Emotional Well-Being

Money issues often lead to significant stress and anxiety. Constant worries about bills, debt, and future expenses can negatively impact your mental health, affecting sleep, relationships, and overall life quality.

Financial stress can result in poor decisions. When overwhelmed, people may make impulsive choices like taking on more debt or making risky investments, worsening their financial situation. This creates a cycle where financial problems cause emotional distress, leading to further financial mistakes.

Ongoing financial stress can significantly impact your well-being, potentially leading to serious mental health issues like depression and anxiety. Additionally, it can manifest as various physical health problems, further complicating your overall health. Addressing financial issues is essential not just for financial stability but for overall well-being.

Coping Mechanisms

Developing strategies to manage financial stress is crucial. Here are some effective coping mechanisms:

Mindfulness: Incorporating practices like meditation into your routine can help you stay centered and composed, leading to more clear-headed and prudent financial decisions. Staying present helps you handle financial matters more effectively.

Therapy: Speaking with a therapist about financial stress can provide you with constructive emotional coping strategies. Therapists can help manage anxiety and develop healthier financial habits. They also help you understand the emotional roots of your financial behaviors.

Financial Education: Educating yourself about personal finance can significantly empower you, enabling you to make smarter decisions and fostering a greater sense of control over your financial future. Reducing fear and uncertainty through education makes financial planning less daunting.

Physical Activity: Regular exercise can significantly reduce stress and elevate your mood. By releasing endorphins, which are natural stress relievers, physical activity provides a constructive outlet for anxiety related to financial issues.

Emotional Support: Reaching out to friends and family allows you to gain emotional support and share your burdens, helping you feel less isolated in your financial struggles. Expressing your financial worries with trusted individuals can offer relief and new perspectives, as well as practical advice and encouragement.

Strategies for Effective Financial Planning

So far, this post has covered a lot of ground in terms of various financial behaviors. Let’s do a quick recap, and bring these dimensions together on what it takes to manage your finances effectively holistically speaking. At a high-level, effective financial planning involves:

Establishing a Budget and Emergency Fund: A detailed budget is key to managing money effectively. Start by listing all income and expenses. Regularly monitor and tweak your budget to make sure it supports your goals and changing circumstances. Prioritizing spending ensures funds go towards your objectives. Building an emergency fund is crucial for unexpected expenses. Aim to save enough for three to six months of living costs. This fund provides a safety net during financial emergencies, reducing the pressure to take on debt.

Setting Long-Term Financial Goals: Focusing on long-term goals like retirement savings or property purchases builds wealth over time. Regular contributions, even small ones, add up significantly. Setting up automatic transfers to savings or investment accounts ensures consistency and helps you stay on track.

Making Short-Term Adjustments (When Needed): Flexibility is important. Making short-term changes, such as reducing discretionary spending or increasing income, can help you stay aligned with your goals. However, it’s crucial to make these adjustments only when necessary and avoid temptations like trend chasing or panic selling. Small, well-considered changes can significantly impact your overall financial health without derailing your long-term plans.

Automating Financial Processes: Simplify your financial management by automating savings, investments, and debt payments. Automated transfers to savings and investment accounts keeps you consistent with contributions without constantly asking for your attention. Establish a systematic debt repayment plan that focuses on high-interest debts first, potentially consolidating loans to reduce interest. Automation helps maintain discipline and fosters long-term financial security.

Creating a Supportive Financial Network: Surrounding yourself with the right people can profoundly influence your financial success. Identify mentors and role models who exemplify sound financial practices and can provide guidance. Foster relationships with family and friends who are supportive of your financial aspirations. Additionally, seek out professional advice from a Certified Financial Planner (CFP®) to receive personalized, expert advice and navigate complex financial decisions with confidence.

Maintaining Holistic Health: Ensuring your mental and physical health is a fundamental aspect of effective financial management. Neglecting your well-being can result in unexpected medical expenses and cloud your judgment when making financial decisions. To bolster your overall health, incorporate regular exercise, nutritious eating, and mindfulness activities like meditation into your everyday schedule. Additionally, consulting with mental health professionals, such as counselors or therapists, can help you manage stress and maintain emotional balance, ultimately leading to more prudent financial choices.

Additional Resources

For those looking to further their financial education, numerous resources can help. If you’re looking for some places to start, I’d recommend checking out some of the following:

“Your Money or Your Life” by Vicki Robin: This pivotal guide redefines how you view and interact with money, aiming to help you achieve true financial independence. It covers in-depth methods for tracking every cent you spend, critically analyzing your expenses, and aligning your financial habits with your core values to create a more purposeful and financially secure lifestyle.

“The Total Money Makeover” by Dave Ramsey: Ramsey’s comprehensive manual offers a detailed, actionable plan to rid yourself of debt, build a substantial emergency fund, and invest wisely for the future. Through inspiring real-life testimonials, he provides practical steps and motivational advice to help you transform your financial situation and achieve long-term stability.

“Rich Dad Poor Dad” by Robert Kiyosaki: Kiyosaki contrasts the financial philosophies of his two father figures to deliver powerful lessons on wealth-building and financial intelligence. The book emphasizes the critical role of financial education, savvy investing, and developing an asset-oriented mindset to pave the way toward substantial financial growth and independence.

“The Psychology of Money” by Morgan Housel: This insightful book explores the psychological underpinnings of how we perceive and manage money. Housel uncovers the often irrational ways people think about wealth, greed, and happiness, offering profound lessons on how these thoughts influence financial decisions and behaviors, ultimately shaping our financial destinies.

“The Millionaire Next Door” by Thomas J. Stanley and William D. Danko: Stanley and Danko unveil the surprising habits and traits of America’s wealthiest individuals, highlighting the importance of frugality, disciplined saving, and wise investing. The book demonstrates that ordinary people can accumulate significant wealth by adopting these practices and living below their means.

“Atomic Habits” by James Clear: Although not solely about finance, Clear’s book provides invaluable strategies for forming good habits and breaking bad ones, which are essential for effective money management. His practical advice on habit formation can help you develop consistent, positive financial behaviors, leading to improved financial health and success over time.

We Can Help

As a CFP® Professional with over 12 years of experience helping clients navigate retirement, I’ve seen firsthand that personal finance is about much more than just numbers and technical knowledge. It’s deeply rooted in behavior. How you handle money, set goals, and deal with stress are critical factors in your financial health. Understanding and addressing the emotional aspects of personal finance can lead to better decision-making.

In my role as a financial thinking partner, I help clients recognize how their emotions and habits influence their spending, saving, and investing. This self-awareness enables the development of disciplined and beneficial financial behaviors, aligning with long-term goals.

Evaluating your financial habits is essential. Setting clear, achievable goals gives you a roadmap for your financial journey. Implementing strategies like budgeting, saving, investing, and debt management can significantly improve your financial health and provide a sense of control.

Now is the perfect time to take action. Assess your financial behaviors, set your goals, and use the tools and strategies we’ve discussed to enhance your financial stability. For personalized guidance, consider scheduling an appointment with a financial advisor. Click the button below to start your journey toward financial stability with expert support.

If you would like us to guide you through this difficult moment instead of going through it alone…

We offer a free consultation called…

The Financial Transition Strategy™

It’s designed to help you quiet the noise and create a clear path forward, as well as help you get to know us and see if we’d be a good fit to work together.

We’re always respectful, and there’s never any pressure.

Securities and advisory services offered through Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Advisor. Fixed insurance products and services not offered through Commonwealth Financial Network®.